Determining Whether an Employee Stock Option Plan Makes Sense

JULY 24, 2024

Planning for private company stock option plans

We frequently work with entrepreneurs and their legal team implementing stock or option ownership plans. Careful consideration of the objectives of the plan and income tax consequences is important at the outset of the plans design.

A stock option plan provides employees with the ability to purchase shares of a company either at the inception of the plan or in the future at a predetermined price. Generally, the idea is that by rewarding members of the leadership team with shares or options the team will be better goal aligned with ownership.

Is employee ownership right for your business?

In a public company setting the concept of offering share linked compensation to employees is well entrenched. The value of the shares and options is easy to assess as the market price is quoted and traded daily. And at the point of vesting the employee can exercise the options and sell their shares.

In the private company context, the lack of marketability of shares means that shares or options are not always the best compensation tool. In our experience, private company ownership works best when ownership is targeting a sale transaction in the medium term and wants to ensure that senior members of the management team are aligned with a successful transaction. We have seen these plans work beautifully with both early stage technology companies and with mature businesses where the founding entrepreneur decides to build an exit strategy. Of course, employee ownership can also work well with many service businesses and in other circumstances where the culture fits. However, its important to think carefully about all of the other tools – salary, benefits and bonus plans – before concluding that ownership is best.

Employee ownership, generally has the following challenges:

- In an ownership situation its important to establish what information that should be shared. If an employee owns shares or options in business they may feel entitled to receive more information that the founder might wish to share.

- A shareholder’s agreement will need to be in place to define the rights of the employee shareholders.

- If an employee leaves prior to exit then the company must raise the funds to pay for the exit of

the employee.

- The employee lacks control over the timing of the transaction that gives rise to the payout – this can lead to unintended consequences including departure to trigger the exit provisions.

What are the key terms of the plan?

Key considerations in establishing your plan include:

- What percentage of the company’s value should be allocated to the plan?

- Which employees should be part of the plan?

- When should the shares be available to the participants? The terms “vested” is generally used here – when can the employee exercise the option and acquire the shares?

- What happens if an employee leaves prior to the sale of the company to a third party?

There is no rule or broad correct answer on the amount of value that should be allocated; however, compensation experts can be retained to help address this question as required. In our experience the one time potential arising from an ownership stake in a private company aiming toward a transaction is a multiple of the employees base compensation – the idea is to create a meaningful upside for the key employee.

Most of our clients have concluded that only the most important contributors to the company should be part of the ownership team. One of the central purposes of the plan is to drive alignment and this is generally most important with the leaders in the organization while other simpler plans can be more effective with the remaining team.

Vesting conditions determine when an employee can exercise their stock option, and can be based on a set timeline - for example, three to five years from the date the options were granted to the employees, with a percentage of the stock options vesting each year. The set period should not be too long or short - too long can often make it out of reach for employees, while having it short may mean that the employee has been gifted the shares rather than earnings the shares over a period of service. Additionally, vesting conditions can be based on the employee meeting certain targets, like revenue growth or other key performance indicators.

Some founders only allow for the vesting upon the occurrence of a “triggering event”. Typically, the triggering event is the sale of the company but it might also include long service.

In the case of an early exit by the employee any unvested options will be forfeited. As the plan is formulated all scenarios need to be carefully considered including such eventualities as early departure for death, disability and leaving to compete. The shareholders’ agreement may well drive vastly different results depending on the circumstances of the employee’s departure.

Tax Planning

The taxation of employee stock options is complex, as there are a number of factors that determine how an employee stock option will be taxed. And, it’s important that business owners understand that if the plan is designed favourably for the employee then the company will not receive any deduction either at the time the employee receives the shares or when the shares are sold by the employee.

Favourable treatments consists of:

- The ability to only pay tax on 50% or 67% of the gain at the time the shares are sold. Prior to June 2024 qualified gains were eligible for a 50% deduction – however as a result of increased inclusion rates for capital gains that occurred in 2024 the deduction is now limited to 33% on everything above $250,000 in a year (and the $250,000 must be shared with other gains realized by an individual in the year the option benefit is realized); and

- Possible use of Canada’s capital gains exemptions which allows individuals to sell qualified Canadian controlled small business shares held for more than two years free of tax for up to $1.25 million. This exemption would only apply to the gain realized after acquiring the actual shares (it does not apply for value that accrued while the employee held options)

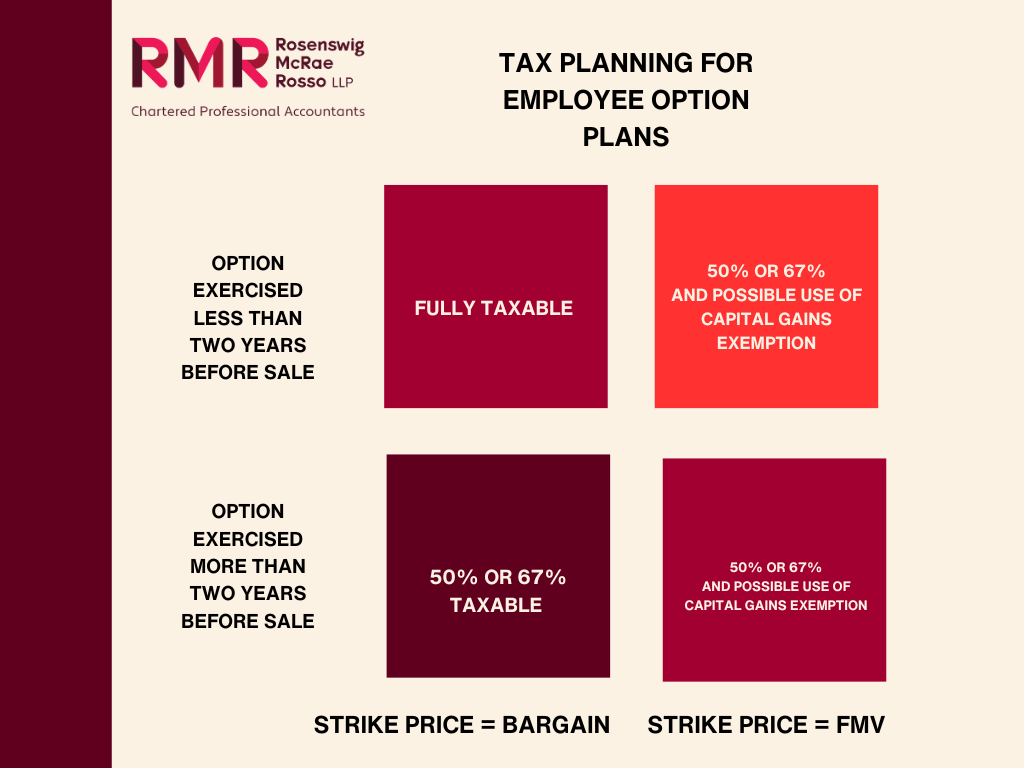

There are two key factors in determining whether an employee receives the ability to only pay tax on 50% or 67% of the gain when they sell the shares. The two key factors are:

1. Was the stock option plan price equal to or greater than the fair market value of the shares at the time the option was granted?

2. Were the actual shares acquired after the exercise of the option held for two years?

So the design of the plan can result in any of the following: a tax free transaction, capital gains like treatment, fully taxable income or a combination!

The answer to these questions drives the tax result as illustrated below:

In all cases where the option plan is carefully designed there is no immediate tax consequences to the employee – the tax only occurs at the time that the shares are disposed of.

For an employee the best situation is that options can be exercised early and they can acquire the actual shares. This will mean that the employee is likely to achieve the 50% or 33% deduction and that they may be able to utilize the capital gains exemption of up to $1.25 million. However, there is a downside – if the company’s value falls then they will receive a T4 benefit for the discount from fair market value on the date of receiving the shares and a capital loss. In our experience this downside is sometimes overstated as there is often the ability to claim an allowable business investment loss provided the company meets the criteria at the time the loss is incurred.

Designing an option plan for your employees is an important task. If you need help thinking through the merits and details of a plan please reach out to a member of our leadership team.